Advantages & Limitations Of Auditing- Here’s an overview of the advantages and limitations of auditing:

Advantages of Auditing

- Enhanced Credibility and Trust:

- Auditing adds credibility to financial statements, increasing stakeholders’ confidence in the accuracy and fairness of the organization’s financial information.

- Fraud Detection and Prevention:

- Auditing can uncover fraudulent activities or irregularities in financial records, acting as a deterrent for employees or management considering unethical actions.

- Compliance with Laws and Regulations:

- Ensures that the organization complies with applicable legal and regulatory frameworks, avoiding penalties and reputational damage.

- Improved Financial Accuracy:

- Identifies errors, misstatements, or omissions in financial records, leading to better financial reporting practices.

- Effective Risk Management:

- Helps organizations identify operational and financial risks, improving internal controls and overall risk management strategies.

- Investor and Lender Confidence:

- Audited financial statements provide assurance to investors and lenders, facilitating access to capital and favorable financing terms.

- Operational Efficiency:

- An audit can highlight inefficiencies and weaknesses in operational processes, offering recommendations for improvement.

- Facilitates Better Decision-Making:

- Reliable and accurate financial data resulting from audits enables management to make informed decisions.

Limitations of Auditing

- Cost-Intensive:

- Auditing can be expensive, particularly for small businesses, due to the fees charged by external auditors and the resources required.

- Time-Consuming:

- Auditing is a lengthy process, which may disrupt daily operations and require significant time commitments from management and staff.

- Scope Limitations:

- Auditors rely on sampling techniques, so there’s always a risk that certain material misstatements or errors may go undetected.

- Dependence on Management Representations:

- Auditors often rely on information provided by management, which can be incomplete or biased, impacting audit quality.

- Not a Guarantee Against Fraud:

- Auditing is designed to provide reasonable, not absolute, assurance. Sophisticated fraud schemes may still go undetected.

- Subjectivity:

- Auditors may exercise professional judgment, which can lead to subjective interpretations, especially in areas like valuations or estimations.

- Limited Focus:

- Financial audits primarily focus on financial data and compliance, often neglecting broader operational or strategic risks.

- Human Errors or Bias:

- Auditors are not immune to errors or bias, which can impact the quality and reliability of the audit report.

If you’d like, I can expand on specific points or suggest ways to mitigate the limitations.

What is Required Advantages & Limitations Of Auditing

When you ask about “Required” advantages and limitations of auditing, I assume you’re referring to the essential or core benefits and drawbacks that are most commonly observed and necessary in the auditing process. Here’s a streamlined version focusing on the most critical advantages and limitations of auditing:

Required Advantages of Auditing

- Increased Credibility of Financial Information:

- The most fundamental advantage is that auditing enhances the reliability and trustworthiness of financial statements, which are essential for stakeholders like investors, lenders, and regulatory bodies.

- Fraud Detection and Risk Mitigation:

- Audits help in detecting discrepancies or fraudulent activities in an organization’s financial records, reducing the risk of financial mismanagement or fraud.

- Legal and Regulatory Compliance:

- Auditing ensures that companies comply with applicable laws, regulations, and standards, preventing legal liabilities and penalties.

- Improvement of Internal Controls:

- Audits assess internal controls and suggest improvements to ensure better operational efficiency and security of assets.

- Investor and Stakeholder Confidence:

- Audited financial statements reassure investors, stakeholders, and the public that an organization is managed properly and that the financial information is accurate.

Required Limitations of Auditing

- Cost and Resource Intensive:

- Auditing, especially external audits, can be expensive, requiring significant financial resources and time, particularly for smaller organizations.

- Sampling Limitations:

- Audits are based on sample testing, meaning that auditors cannot review every transaction or financial record, which could leave room for errors or fraud.

- Not a Guarantee of Absolute Accuracy:

- Auditing provides reasonable assurance rather than absolute certainty that financial statements are free from error or fraud, so some issues may go undetected.

- Dependency on Management Information:

- Auditors rely heavily on information provided by management, and inaccuracies or intentional misrepresentation by management could compromise the audit’s effectiveness.

- Limited to Financial Scope:

- Traditional audits primarily focus on financial data and compliance, and often overlook broader business issues such as operational or strategic performance.

These core advantages and limitations form the foundation of auditing’s role and function in business and organizational settings.

Who is Required Advantages & Limitations Of Auditing

Here’s a breakdown of who needs to be aware of these advantages and limitations:

Who Requires Knowledge of the Advantages & Limitations of Auditing?

- Business Owners and Management:

- Business leaders need to understand the advantages of auditing to ensure that their financial reporting is accurate, compliant, and trustworthy. At the same time, they must be aware of the limitations to properly manage expectations and plan resources.

- Internal Auditors:

- Internal auditors must fully grasp the benefits of audits (like improving internal controls) and the limitations (such as sampling methods) in order to conduct effective internal audits and contribute to continuous improvements.

- External Auditors:

- External auditors must be aware of both the advantages and limitations to ensure they perform audits that are thorough, comply with standards, and meet the needs of stakeholders. They also need to be prepared to address limitations, such as reliance on management information or sampling.

- Investors and Shareholders:

- Investors and shareholders rely on audited financial statements to make informed decisions. Understanding the advantages helps them trust the financial reports, while knowledge of limitations allows them to be aware of the potential gaps in audit coverage.

- Regulators and Government Agencies:

- Regulatory bodies, such as the Securities and Exchange Commission (SEC) or tax authorities, require audits to ensure compliance with laws. They must understand both advantages (like detecting fraud) and limitations (like the inability to guarantee fraud detection) to assess audit quality and effectiveness.

- Creditors and Lenders:

- Lenders, such as banks or financial institutions, often require audited financial statements when making loan decisions. Understanding the auditing process helps them interpret financial reports more accurately and mitigate risks when extending credit.

- Employees:

- While employees may not directly conduct audits, they benefit from understanding audits’ role in ensuring fairness and transparency in the organization, especially in terms of internal controls and protecting the company’s financial health.

- Consultants and Advisors:

- Business consultants, financial advisors, and other professionals who provide strategic or financial advice need to understand both the benefits and limits of audits to offer the most informed recommendations.

- Suppliers and Business Partners:

- Suppliers and business partners may require audits to verify the financial stability and trustworthiness of their partners before entering into long-term agreements or contracts.

In Summary:

The required stakeholders for understanding the advantages and limitations of auditing include:

- Business owners, management, and auditors (internal and external)

- Investors, regulators, creditors, and financial institutions

- Employees and business partners who rely on accurate and credible financial data

Each group benefits from understanding auditing’s value while managing expectations regarding its limitations.

When is Required Advantages & Limitations Of Auditing

Here’s a breakdown of the key times when understanding the advantages and limitations of auditing is crucial:

When Are the Advantages of Auditing Relevant?

- During Financial Reporting Periods:

- Annual Reports: The advantages of auditing are most relevant when organizations are preparing their annual financial statements. An audit ensures that these reports are accurate and credible, helping to gain stakeholders’ trust.

- Quarterly Reports: Even for quarterly reports, an internal or external audit can provide assurance that the financial data is correct and in line with regulatory requirements.

- When Seeking External Funding:

- Investors: When a company is seeking investment or issuing stocks, investors look for audited financial statements to make informed decisions.

- Lenders and Creditors: Banks and other lending institutions often require audited financials before granting loans or extending credit to ensure the company is financially stable.

- During Mergers and Acquisitions (M&A):

- Due Diligence: When companies are involved in mergers, acquisitions, or joint ventures, audits are critical in verifying the accuracy of financial statements, which influences the negotiation process and final agreement.

- When Ensuring Legal and Regulatory Compliance:

- Legal Requirements: Organizations subject to regulatory bodies (e.g., SEC for public companies) are required to have their financials audited to ensure compliance with financial reporting standards and laws.

- During Strategic Decision-Making:

- Management Decisions: Business leaders rely on the insights from audits to make informed strategic decisions, improve internal controls, and address potential operational issues.

- To Detect Fraud or Irregularities:

- Fraud Detection: The advantage of detecting fraud is particularly relevant when there’s suspicion of financial mismanagement, or when implementing a robust anti-fraud framework within an organization.

- When Planning for Long-Term Business Growth:

- Risk Management: Auditing helps identify risks and inefficiencies that could impact long-term business planning and sustainability, allowing businesses to take proactive steps.

When Are the Limitations of Auditing Relevant?

- When Interpreting Audit Reports:

- Auditors’ Report: Stakeholders, such as investors or regulators, need to understand the limitations of auditing when interpreting audit reports. For example, the audit opinion is based on reasonable assurance, meaning some errors or fraud might still go undetected.

- During Fraud or Error Detection:

- Risk of Undetected Fraud: Auditing can only catch issues that are within the scope of the audit process. If fraud is sophisticated or well-hidden, it may not be detected, making it important for stakeholders to understand this limitation.

- When Planning Audit Scope and Resources:

- Sampling Limitations: Auditors rely on sampling, which means they don’t check every transaction. This limitation is important when auditors and management are planning the audit scope and ensuring that resources are allocated appropriately.

- Management Representations: Auditors depend on the information provided by management, so any intentional misrepresentation or oversight can lead to inaccuracies in the audit.

- During Budgeting and Resource Allocation:

- Cost Implications: Understanding the costs involved in an audit is crucial for business owners and management, especially when deciding between internal or external audits or considering alternative forms of assurance.

- When Evaluating Audit Results in Complex Organizations:

- Limited Scope of Audit: For very large, complex organizations or multinational companies, the audit process might not cover every subsidiary or operational area. Stakeholders need to be aware of this limitation when making decisions based on audit results.

- When Dealing with Internal Control Weaknesses:

- Inadequate Internal Controls: If an organization’s internal controls are weak, an audit may not be able to uncover all operational issues. Recognizing this limitation helps organizations take steps to improve their control systems.

- When Understanding Audit Assurance:

- Reasonable vs. Absolute Assurance: Auditing provides reasonable assurance, not absolute certainty. This is important when stakeholders are deciding how much trust to place in the audit findings and whether they need further checks.

Summary:

The advantages and limitations of auditing are relevant:

- During the preparation of financial reports and seeking investment or loans

- In the due diligence process of mergers and acquisitions

- For legal compliance and fraud detection

- For decision-making regarding risk management and operational efficiency

The limitations become important:

- When interpreting audit results, especially in cases of fraud or when relying on management representations

- During audit planning (e.g., understanding sampling limitations)

- When budgeting for audits and evaluating their cost-effectiveness

Where is Required Advantages & Limitations Of Auditing

Here’s an overview of where auditing’s advantages and limitations come into play:

Where Are the Advantages of Auditing Relevant?

- In Financial Reporting:

- Publicly Listed Companies: Companies listed on stock exchanges are required by regulators (such as the SEC in the U.S.) to have their financial statements audited, making the advantages of auditing crucial in maintaining investor confidence.

- Private Companies: Even though private companies are not always required to undergo an audit, those that do benefit from the credibility audits bring to their financial reports, which can be crucial for securing investment or loans.

- In Regulatory and Legal Environments:

- Government and Regulatory Bodies: Regulatory agencies, such as the IRS or national securities commissions, require audits to ensure that organizations comply with financial reporting laws and regulations, which promotes transparency and accountability.

- Tax Authorities: Auditing helps businesses comply with tax laws by verifying the accuracy of tax returns and financial statements, reducing the risk of tax fraud or underreporting.

- In Financial Markets:

- Stock Markets: Investors rely on audited financial statements to make informed decisions about buying or selling stocks. The audit provides assurance that the financials are accurate, helping prevent market manipulation or misinformation.

- Banks and Financial Institutions: Lenders require audited financial statements to assess the creditworthiness of businesses, ensuring they can repay loans and manage their financial obligations.

- In Risk Management and Internal Controls:

- Internal Audit Departments: Many large organizations have internal audit departments that perform audits to identify inefficiencies, weak controls, and potential areas of risk. The advantage here is improving internal processes and mitigating future risks.

- Compliance Officers: Compliance officers rely on audits to ensure that the company adheres to relevant laws and internal policies, protecting the organization from legal or financial penalties.

- In Mergers, Acquisitions, and Due Diligence:

- Mergers and Acquisitions (M&A): Audits are critical during M&A due diligence, ensuring that the financial health of the company being acquired is accurately assessed. The audit provides a clear view of liabilities, assets, and risks involved in the transaction.

- Investment Analysis: Investors or venture capitalists conducting due diligence on potential investments look to audited financial statements to assess the financial health and risks of a company.

- In Business Growth and Expansion:

- Strategic Planning: Business leaders rely on audit results to identify growth opportunities and potential operational weaknesses, making it essential for long-term business planning and expansion.

Where Are the Limitations of Auditing Relevant?

- In Financial Reporting and Analysis:

- Interpretation of Audit Reports: The limitations of auditing are most evident when interpreting audit reports. Stakeholders (like investors or creditors) must understand that an audit only provides reasonable assurance and does not guarantee the absolute accuracy of the financial statements.

- Complex Organizations: In large organizations or multinational corporations, audits may not cover every aspect of the business, leading to the possibility of missed risks or issues that are outside the scope of the audit.

- In Risk Management and Internal Controls:

- Weak Internal Controls: If an organization has weak internal controls, an audit might not uncover all issues. For example, an auditor may not detect fraud if the fraudulent activities are well-hidden or circumventing internal controls.

- Sampling Limitations: Auditors rely on sample testing rather than checking every transaction, meaning that some discrepancies may go undetected. This limitation is particularly relevant in industries or sectors where large volumes of transactions are involved.

- In Fraud Detection:

- Sophisticated Fraud Schemes: The limitations of auditing are crucial to consider when dealing with complex or sophisticated fraud schemes. Audits are not designed to guarantee the detection of fraud, especially if the fraud is well-hidden or involves collusion among employees.

- Reliance on Management Representations: Auditors depend on information provided by management, so if management misrepresents data or withholds critical information, fraud or errors may go undetected.

- In Legal and Compliance Areas:

- Compliance Gaps: Audits help ensure compliance with laws, but they do not cover every legal aspect of a business. The limitation here is that auditors cannot always detect non-financial regulatory violations or fully ensure that all legal requirements are met.

- In Cost-Benefit Analysis for Audits:

- Small to Medium Enterprises (SMEs): For small businesses, the costs of an audit might outweigh the benefits, especially if they are not legally required to undergo one. The limitation here is the resource drain on the organization for what may be an unnecessary procedure.

- Limited Audit Scope: Auditors have a defined scope and may not be able to address every aspect of the organization, especially when resources are limited or when the audit is only partial.

- In Decision-Making:

- Dependence on Audit Findings: Business leaders, investors, or creditors who base decisions solely on audit findings may overlook certain nuances due to the audit’s limitations (e.g., areas outside the audit scope or limitations in sampling).

Summary:

The advantages of auditing are relevant in:

- Financial reporting, risk management, legal compliance, and investment decisions.

- Mergers, acquisitions, and due diligence processes, where trust in financial information is crucial.

The limitations of auditing are relevant in:

- Risk management when audits fail to detect fraud or inaccuracies.

- Financial analysis where an audit cannot guarantee absolute accuracy or cover all areas.

- Small businesses where the audit might be costly relative to the benefits.

How is Required Advantages & Limitations Of Auditing

Here’s a breakdown of how the advantages and limitations of auditing impact different stakeholders and processes:

How Are the Advantages of Auditing Realized?

- Enhancing the Credibility of Financial Statements:

- How: Auditing provides an independent and professional review of a company’s financial statements, ensuring that they reflect a true and fair view of the company’s financial position. This is particularly crucial for businesses that want to gain the trust of investors, creditors, and regulatory bodies.

- Example: A publicly listed company undergoes an audit, which increases the credibility of its financial reports, reassuring investors that the data is accurate and compliant with regulations.

- Fraud Detection and Prevention:

- How: Auditors examine financial records and internal controls to detect signs of fraud or financial mismanagement. While they may not guarantee that fraud will be found, audits help minimize the risk of undetected fraudulent activities.

- Example: Auditors uncover discrepancies or suspicious transactions that indicate potential fraud, leading to internal investigations and corrective measures.

- Legal and Regulatory Compliance:

- How: Audits help businesses comply with laws and regulations such as tax laws, financial reporting standards, and industry-specific rules. Compliance ensures the organization avoids legal issues or penalties.

- Example: A company undergoing an audit to meet regulatory requirements (such as SEC filings for public companies) ensures it complies with reporting standards and avoids penalties.

- Improving Internal Controls:

- How: Auditors assess the effectiveness of internal controls and suggest improvements to reduce risks, enhance operational efficiency, and safeguard assets.

- Example: During an audit, an auditor finds weaknesses in the company’s internal controls, such as poor segregation of duties, and recommends changes to strengthen the system.

- Investor and Stakeholder Confidence:

- How: Reliable financial statements that are audited provide assurance to investors, shareholders, and stakeholders, ensuring that they have access to accurate and truthful information, which helps them make informed decisions.

- Example: An investor is more likely to invest in a company with audited financial statements because it gives them confidence in the company’s financial health.

How Are the Limitations of Auditing Realized?

- Sampling Limitations:

- How: Auditors typically do not examine every transaction in detail. They rely on sampling methods to draw conclusions about the financial statements. This means there’s a possibility that some errors or fraud may go undetected.

- Example: In a large company, an auditor may sample only a portion of the transactions rather than reviewing every single one. If fraudulent activities are limited to unsampled transactions, they may not be discovered.

- Reasonable Assurance, Not Absolute Certainty:

- How: Auditors provide reasonable assurance that the financial statements are free from material misstatements, but they cannot guarantee complete accuracy. There’s always a chance that some issues will be missed.

- Example: An audit might fail to identify small but material misstatements that could affect the decisions of stakeholders.

- Dependence on Management Information:

- How: Auditors rely on the information provided by company management. If management is not transparent or intentionally misrepresents data, it could lead to an incomplete or inaccurate audit.

- Example: If management provides incomplete financial records or misleads the auditor about certain transactions, the auditor may miss critical errors or fraud.

- Limited Scope:

- How: Audits are usually limited to reviewing financial statements and internal controls. They do not typically address non-financial areas such as operations, market conditions, or strategic risks, which could affect a company’s overall performance.

- Example: An audit may focus on the accuracy of financial data but does not analyze the company’s operational inefficiencies, which could lead to cost overruns or missed revenue opportunities.

- Not Designed to Detect Fraud in All Cases:

- How: While audits are designed to detect fraud, they are not foolproof. Highly sophisticated fraud schemes may evade detection, especially if they involve collusion or manipulation of internal controls.

- Example: A company may be involved in a complex fraudulent scheme that manipulates financial records in such a way that it’s not easily identified during a routine audit.

- Time and Cost Constraints:

- How: Auditing is a resource-intensive process, involving time, personnel, and costs. The audit process might be limited by these factors, meaning that auditors may focus on the most material areas, potentially leaving others under-examined.

- Example: Due to budget or time constraints, auditors may not be able to perform extensive testing or review every aspect of the company’s financial situation, leading to possible gaps in their findings.

How the Advantages and Limitations Impact Stakeholders:

- Business Owners and Management:

- Advantages: They gain insights into the accuracy of their financial reporting, internal controls, and areas for operational improvement.

- Limitations: They need to be aware of audit costs, the potential for undetected issues, and the fact that not all areas of the business are reviewed in detail.

- Investors and Creditors:

- Advantages: They rely on audits to make informed decisions about a company’s financial stability and growth potential.

- Limitations: They must understand that audits are not foolproof and that certain financial risks might remain undiscovered.

- Regulatory Bodies:

- Advantages: They use audits to ensure companies are complying with legal and regulatory requirements.

- Limitations: They must acknowledge that audits may not catch all instances of non-compliance or fraud, especially in complex cases.

- Auditors:

- Advantages: They ensure that financial statements are accurate and that internal controls are working properly.

- Limitations: They are constrained by factors like time, scope, and reliance on management’s information, which can affect the thoroughness of their audit.

Summary:

The advantages of auditing are realized when the process:

- Enhances financial credibility, ensures compliance, detects fraud, improves internal controls, and builds trust with investors.

The limitations of auditing are felt when:

- Audits rely on sampling, cannot guarantee absolute accuracy, depend on management’s data, and are limited in scope and cost, meaning that some risks or errors might not be detected.

Understanding both how the advantages and limitations manifest allows stakeholders to better interpret audit results and plan accordingly.

Case Study on Advantages & Limitations Of Auditing

Courtesy: Accounts with chandra

Here’s a case study illustrating the advantages and limitations of auditing in a real-world business context:

Case Study: The XYZ Corporation Audit

Company Overview:

XYZ Corporation is a mid-sized manufacturing company that produces consumer electronics. Over the past few years, the company has grown rapidly, expanding into international markets. Due to its growth, XYZ decided to undergo an annual external audit to ensure compliance with financial reporting regulations and to maintain the trust of investors and creditors. The company hired an external audit firm, ABC Auditors, to conduct this audit.

Advantages of Auditing in XYZ Corporation’s Case:

- Increased Credibility of Financial Statements:

- Scenario: XYZ Corporation’s financial statements were prepared for the fiscal year, and potential investors were interested in the company’s growth prospects. XYZ needed to demonstrate the reliability of its financial reporting.

- Audit Benefit: ABC Auditors reviewed the company’s books, and after completing the audit, they issued an unqualified audit opinion. This indicated that the financial statements presented a true and fair view of the company’s financial position.

- Result: The audit helped increase investor confidence, and XYZ was able to secure additional funding from investors, which supported further expansion into new markets.

- Fraud Detection and Prevention:

- Scenario: The company had experienced significant growth, and with that growth came a higher volume of financial transactions and an increase in the complexity of operations. There were concerns that potential fraud could occur, especially in inventory management.

- Audit Benefit: ABC Auditors performed a thorough review of the company’s internal controls and transaction records, focusing on areas where fraud could arise, such as inventory reporting. They found that discrepancies in inventory reporting existed due to inefficiencies in stock tracking.

- Result: The auditors suggested changes to improve inventory tracking and enhance internal controls. The company took corrective actions, reducing the risk of future fraud.

- Improvement of Internal Controls:

- Scenario: XYZ Corporation had rapidly scaled its operations, but management was concerned about the adequacy of the internal control systems, especially in managing cash flows and protecting assets.

- Audit Benefit: The audit uncovered several weaknesses in the company’s internal controls, including inadequate segregation of duties in the finance department and insufficient monitoring of cash flows.

- Result: ABC Auditors recommended improvements, such as the implementation of stronger checks and balances, more robust cash flow monitoring, and automated systems for tracking expenses. These changes enhanced operational efficiency and reduced the risk of mismanagement.

- Regulatory and Legal Compliance:

- Scenario: As XYZ Corporation expanded into international markets, it faced increased scrutiny from regulatory bodies in multiple countries. The company needed to ensure that it was in compliance with global accounting standards and tax regulations.

- Audit Benefit: The external audit assessed whether XYZ Corporation adhered to all relevant financial regulations, including tax laws and international accounting standards. The audit report confirmed the company’s compliance, reducing the risk of legal issues or penalties.

- Result: With the audit confirming compliance, XYZ Corporation was able to continue its international expansion without concerns over legal and regulatory repercussions.

Limitations of Auditing in XYZ Corporation’s Case:

- Sampling Limitations:

- Scenario: XYZ Corporation processed thousands of transactions each day, making it impractical for the auditors to review every transaction in detail. ABC Auditors decided to rely on sampling methods to evaluate the accuracy of the company’s financial data.

- Audit Limitation: The auditors reviewed a sample of transactions, but some transactions, particularly in areas like sales returns and employee reimbursements, were not included in the sample. As a result, there was a chance that errors or fraud in those areas were missed.

- Result: While the audit provided reasonable assurance, it could not guarantee that every error or irregularity was detected. XYZ Corporation had to acknowledge that the sampling method meant that some areas might not have been thoroughly reviewed.

- Dependence on Management Information:

- Scenario: XYZ Corporation provided all necessary financial data to ABC Auditors, including sales reports, expense records, and inventory data. However, management had to prepare and present these records, and there was always the risk of data inaccuracies or incomplete information being provided.

- Audit Limitation: In this case, the auditors relied heavily on the financial information given by management. If there were intentional misstatements or omissions in the records, they might go unnoticed during the audit process.

- Result: The audit report did not uncover any major discrepancies, but the limitation is that it was dependent on the integrity of the management-provided data. If management had withheld or misrepresented information, the auditors may not have detected it.

- Limited Scope of the Audit:

- Scenario: The scope of the audit was focused primarily on the financial statements, internal controls, and regulatory compliance. However, the company also faced challenges in areas like operational efficiency and strategic decision-making.

- Audit Limitation: The audit report did not cover non-financial aspects such as operational performance, market positioning, or management decisions outside of financial matters. For example, the audit didn’t identify inefficiencies in the production process or missed opportunities for cost reduction in certain areas.

- Result: Although the audit improved XYZ Corporation’s financial transparency and compliance, it did not address all the company’s operational challenges. As a result, management had to seek external advice for improving operational efficiency and strategic planning.

- Not Designed to Detect All Fraud:

- Scenario: Given the company’s rapid expansion and increasing complexity, there was concern about potential fraud, particularly in the procurement process and vendor relationships.

- Audit Limitation: While the audit focused on areas where fraud was most likely to occur, it could not guarantee the detection of all fraudulent activities, especially those involving collusion between employees and vendors.

- Result: No fraud was uncovered during the audit, but the limitation is that the audit process may not have detected fraud that was well-hidden or sophisticated. XYZ Corporation needed to implement additional fraud prevention measures beyond the scope of the audit.

Conclusion:

In this case study of XYZ Corporation, the advantages of auditing were evident in enhancing the credibility of financial statements, detecting and preventing fraud, improving internal controls, and ensuring regulatory compliance. These advantages helped the company build trust with investors, manage risks, and make more informed decisions.

However, the limitations of auditing were also apparent. The use of sampling meant that some errors could go undetected, the audit was dependent on the information provided by management, and its scope was limited to financial matters. These limitations meant that XYZ Corporation needed to be aware that the audit did not guarantee absolute accuracy or uncover all potential issues, particularly in non-financial areas or more sophisticated fraud schemes.

Key Takeaways:

- Auditing is a valuable tool for improving transparency, trust, and operational efficiency.

- However, it has inherent limitations, such as reliance on sampling, potential for undetected fraud, and a limited scope that focuses on financial reporting rather than broader business issues.

This case study shows how understanding both the advantages and limitations of auditing can help businesses like XYZ Corporation make better decisions, while also recognizing the need for complementary measures beyond the audit process.

White paper on Advantages & Limitations Of Auditing

Introduction

Auditing is a crucial process that helps to ensure the accuracy, transparency, and reliability of financial statements, internal controls, and organizational practices. Whether conducted internally or externally, audits play a vital role in providing stakeholders with confidence in an organization’s financial health and compliance with laws and regulations. However, like any process, auditing comes with both advantages and limitations that can influence its effectiveness and the value it provides to businesses, investors, regulators, and other stakeholders.

This white paper explores the advantages and limitations of auditing, offering insights into how audits are conducted, the benefits they provide, and the challenges they present.

1. Advantages of Auditing

1.1 Enhanced Credibility and Transparency

One of the primary advantages of auditing is that it enhances the credibility and transparency of a company’s financial statements. Audited financial statements provide an independent, third-party verification of the financial data, assuring stakeholders that the financial records are accurate and in compliance with accounting standards. This is especially important for publicly traded companies, which rely on audited financial statements to maintain investor confidence and comply with regulatory requirements.

Example: Publicly listed companies are required by regulatory bodies (e.g., the SEC in the U.S.) to submit audited financial reports annually. These reports offer a transparent and credible picture of the company’s financial health, which is essential for attracting and maintaining investor trust.

1.2 Fraud Detection and Prevention

Audits are designed to detect and prevent fraud by reviewing financial transactions and internal controls. Auditors assess the company’s processes to identify weaknesses or areas where fraud could occur. While audits cannot guarantee the detection of fraud, they act as a deterrent by ensuring that organizations have robust controls and systems in place.

Example: A company’s internal audit reveals discrepancies in the financial records, prompting further investigation that uncovers embezzlement by an employee. The audit process identifies weaknesses in internal controls, allowing the company to implement corrective measures to prevent future fraud.

1.3 Regulatory and Legal Compliance

Auditing ensures that organizations comply with relevant laws, regulations, and accounting standards. By conducting regular audits, companies demonstrate their commitment to adhering to financial reporting standards (e.g., GAAP, IFRS) and other legal requirements, such as tax regulations. This reduces the risk of legal and regulatory penalties.

Example: A company conducts an external audit to verify its compliance with the Foreign Corrupt Practices Act (FCPA), ensuring that all transactions are legally compliant and that the company is not exposed to the risk of financial penalties.

1.4 Improvement of Internal Controls

Auditors evaluate the effectiveness of internal controls, which are the procedures and systems put in place to safeguard assets, prevent fraud, and ensure operational efficiency. Through the audit process, weaknesses or inefficiencies in these controls are identified, providing an opportunity for businesses to strengthen them.

Example: An auditor identifies inadequate segregation of duties in the accounts payable process, which could lead to misappropriation of funds. The company then restructures its processes, improving internal controls and mitigating the risk of future errors.

1.5 Investor and Stakeholder Confidence

For investors, creditors, and other stakeholders, audited financial statements provide assurance that a company’s financial position is accurately presented. Auditing builds trust, which is crucial for maintaining or securing investments, securing loans, or entering into partnerships. Without audits, stakeholders may be reluctant to trust the company’s financial data.

Example: A company looking to raise capital through an initial public offering (IPO) undergoes a rigorous audit to provide potential investors with reliable and trustworthy financial statements. The audited statements increase investor confidence and contribute to a successful IPO.

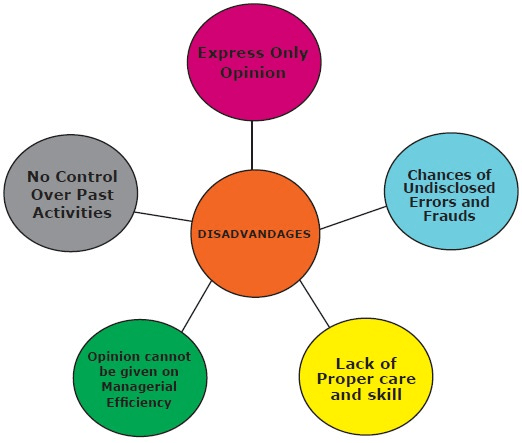

2. Limitations of Auditing

2.1 Sampling Limitations

One of the inherent limitations of auditing is that auditors rely on sampling methods to evaluate financial transactions, especially in large organizations with high volumes of transactions. This means that not all transactions are reviewed, and some errors, fraud, or irregularities could go undetected.

Example: In a large manufacturing company, the auditor may examine only a sample of purchase orders and payments. If fraudulent activities occur in the unsampled transactions, they may not be identified during the audit.

2.2 Reasonable Assurance, Not Absolute Certainty

Auditing provides reasonable assurance, but not absolute certainty, that the financial statements are free from material misstatements. There are inherent risks in the audit process, including human error, incomplete information, or fraudulent activities that are well-concealed. Thus, while an audit helps ensure accuracy, it does not guarantee it.

Example: An audit may detect an error in a financial statement, but it cannot provide complete assurance that all financial data is flawless. The auditor’s opinion is based on professional judgment, and they acknowledge that some degree of uncertainty remains.

2.3 Dependence on Management Information

Auditors rely on the information provided by company management during the audit process. If the management provides inaccurate, incomplete, or misleading information, the auditor’s conclusions and opinion could be compromised. While auditors perform procedures to verify the accuracy of the data, they cannot uncover intentional misstatements if the data provided is deliberately misleading.

Example: A company’s management provides the auditor with a fabricated inventory report. Despite the audit procedures, the auditor may not be able to detect the fraudulent data if it is well concealed.

2.4 Limited Scope of the Audit

Audits generally focus on financial statements, internal controls, and regulatory compliance. However, they do not typically cover non-financial aspects of an organization, such as operational performance, strategic decisions, or market dynamics. As a result, audits may not uncover inefficiencies or risks that affect the broader business environment.

Example: A company’s audit identifies issues with financial reporting and internal controls but does not assess the effectiveness of its marketing strategies or operational processes. As a result, the audit does not identify inefficiencies that could impact the company’s competitiveness.

2.5 Not Designed to Detect All Fraud

Audits are not specifically designed to detect fraud in all cases. While auditors assess the risk of fraud and focus on areas where fraud is most likely to occur, they do not guarantee that all fraud will be uncovered. Fraud detection depends on the type of fraud, the complexity of the fraud scheme, and the quality of internal controls in place.

Example: A company with strong internal controls may still be at risk for sophisticated fraud, such as collusion between employees or vendors. Despite the audit process, such fraud may go undetected if it involves complex manipulation of records.

2.6 Time and Resource Constraints

Auditing is a time-consuming and resource-intensive process. Auditors often have limited time to conduct their review, particularly during busy periods, such as year-end reporting. As a result, the audit may not cover every detail or address all potential risks, especially in large organizations or complex industries.

Example: An audit of a multinational corporation may be constrained by time and budget limitations, leading the auditors to focus on material risks and key financial areas, potentially overlooking smaller but significant issues.

3. Conclusion

Auditing plays a critical role in ensuring transparency, building trust with stakeholders, and identifying areas for operational and financial improvement. The advantages of auditing—such as enhanced credibility, fraud detection, legal compliance, and improved internal controls—help organizations maintain the confidence of investors, regulatory bodies, and other stakeholders.

However, limitations such as sampling constraints, reliance on management information, and the inability to guarantee the detection of all fraud must be acknowledged. These limitations highlight the importance of understanding the scope of an audit and the need for complementary measures, such as robust internal controls, fraud prevention programs, and additional due diligence by management and stakeholders.

To maximize the benefits of auditing, companies must recognize the potential gaps in the audit process and implement proactive strategies to mitigate risks beyond the scope of the audit itself.

Recommendations

- For Organizations: While audits provide valuable insights, companies should also invest in strong internal controls, regular risk assessments, and fraud prevention mechanisms to complement the audit process.

- For Auditors: It is important for auditors to communicate the limitations of audits clearly to stakeholders and provide transparency about the scope and methods used in the audit process.

- For Stakeholders: Investors, creditors, and other stakeholders should be aware of the limitations of auditing and use audited financial statements in conjunction with other forms of due diligence.

Industrial Application of Advantages & Limitations Of Auditing

Auditing is a critical function across all industries, offering significant advantages in enhancing financial accuracy, trust, and compliance. However, its limitations also shape how industries approach auditing and rely on other tools to manage risks and ensure operational success. In this section, we explore how the advantages and limitations of auditing are applied within different industries and sectors.

1. Manufacturing Industry:

Advantages in the Manufacturing Sector:

- Improved Internal Controls:

- Application: In the manufacturing industry, companies often deal with complex supply chains, large volumes of raw materials, and extensive inventories. Auditors assess internal controls over these areas, ensuring that inventory is accurately tracked, and production costs are properly recorded.

- Example: A manufacturing company might be audited to verify that their inventory management system is functioning correctly, which helps prevent stock losses or overstatement of assets.

- Benefit: This strengthens internal controls, reduces fraud risks, and enhances efficiency by ensuring accurate financial reporting of production and raw material costs.

- Fraud Detection and Prevention:

- Application: Audits in the manufacturing sector focus on areas where fraud is likely to occur, such as procurement and inventory management. Fraudulent activities like inflating inventory levels or skimming from supplier payments can be detected through auditing.

- Example: An auditor uncovers discrepancies in the company’s inventory records, leading to the discovery of fraudulent invoicing for goods that were never received.

- Benefit: Early detection of fraud helps to protect the company’s financial resources and preserve its reputation.

- Regulatory Compliance:

- Application: Manufacturing companies are subject to a range of regulations regarding product safety, environmental compliance, and financial reporting standards (such as GAAP or IFRS). Audits ensure that the company is in compliance with these regulations.

- Example: An audit reveals that the company has not been properly documenting environmental compliance, which is crucial to avoid fines or sanctions.

- Benefit: Compliance audits help avoid legal penalties and demonstrate the company’s commitment to regulatory adherence.

Limitations in the Manufacturing Sector:

- Sampling Limitations:

- Application: Due to the high volume of transactions in the manufacturing industry, auditors typically rely on sampling to review financial records. While sampling can provide an overview, it cannot guarantee that all discrepancies or irregularities are detected.

- Example: An auditor reviews only a small sample of purchase orders, but fraudulent activities might have occurred in the unsampled transactions.

- Limitation: This may result in undetected errors or fraud in less-scrutinized areas.

- Complexity of Supply Chains:

- Application: The complexity of global supply chains in the manufacturing sector makes it difficult for auditors to review every transaction or verify the entire supply chain.

- Example: The auditor might focus on the company’s financial statements but cannot fully verify the accuracy of global procurement or payments to suppliers in different countries.

- Limitation: Due to logistical challenges, the audit may miss inconsistencies or fraud in foreign suppliers or outsourced operations.

2. Financial Services Industry:

Advantages in the Financial Services Sector:

- Investor Confidence:

- Application: Audited financial statements in financial institutions (e.g., banks, insurance companies, investment firms) provide investors, regulators, and clients with confidence in the company’s financial health.

- Example: A publicly traded bank undergoes an audit, which increases investor confidence in its financial stability and ability to meet regulatory requirements.

- Benefit: This results in enhanced trust, higher stock prices, and greater investment in the firm.

- Regulatory Compliance and Legal Protection:

- Application: The financial services industry is highly regulated, with institutions needing to comply with stringent reporting requirements, anti-money laundering laws, and financial stability rules. Auditors verify that these institutions adhere to regulations and provide an accurate representation of their financial health.

- Example: A bank undergoes an audit to ensure compliance with Basel III regulations on capital adequacy, liquidity, and leverage.

- Benefit: Compliance audits prevent legal penalties and reputational damage, ensuring that institutions can operate smoothly in a heavily regulated environment.

- Risk Management:

- Application: In financial services, auditors assess the risk management practices of institutions. They review the processes for credit risk, market risk, operational risk, and compliance risk, ensuring that risks are appropriately mitigated.

- Example: An audit of a financial institution’s credit portfolio identifies high concentrations of risky loans, prompting the institution to diversify its lending practices.

- Benefit: Effective risk management helps prevent major financial losses and ensures the institution’s long-term sustainability.

Limitations in the Financial Services Sector:

- Complex Financial Instruments:

- Application: The financial services sector deals with complex financial instruments such as derivatives, structured products, and securitized assets. Auditors may find it challenging to fully assess the risk or valuation of these instruments.

- Example: An auditor may not fully understand the complexities of a derivatives portfolio or hedge strategies, limiting their ability to assess the accuracy of financial statements related to these instruments.

- Limitation: This can result in incomplete assessments of financial risk or valuations, potentially leading to inaccuracies in the audit report.

- Dependence on Management Information:

- Application: Auditors in the financial services industry rely on the financial data provided by management, which may involve subjective judgments, such as assumptions in asset valuations and provisions for bad loans.

- Example: A bank’s management provides an estimate of the credit risk related to a loan portfolio, which is based on subjective models and assumptions that might not be fully verified during the audit.

- Limitation: If management’s estimates are inaccurate or overly optimistic, it can affect the auditor’s conclusions and the reliability of the financial statements.

3. Healthcare Industry:

Advantages in the Healthcare Sector:

- Improved Financial Management:

- Application: Healthcare organizations, including hospitals and insurance companies, are often subject to significant financial regulation. Auditing helps ensure the accuracy of billing, reimbursement, and expense tracking.

- Example: An audit of a healthcare provider’s billing practices reveals inefficiencies and overbilling, which leads to improved cost management and better pricing transparency for patients.

- Benefit: Better financial management and cost control, improving the healthcare organization’s bottom line.

- Compliance with Healthcare Regulations:

- Application: Healthcare organizations must comply with strict regulations, including the Health Insurance Portability and Accountability Act (HIPAA), as well as Medicare and Medicaid reporting requirements. Audits verify that these entities are in compliance.

- Example: A hospital undergoes an audit to ensure compliance with Medicare billing rules and to verify that they are not overcharging or misreporting claims.

- Benefit: Compliance audits help avoid regulatory fines and ensure that the healthcare provider remains eligible for government reimbursements.

- Risk Mitigation in Healthcare Transactions:

- Application: Audits help healthcare providers manage risk by ensuring that financial transactions, patient billing, and insurance claims are accurate, reducing the risk of fraud and legal disputes.

- Example: An audit reveals that a hospital’s insurance claims department is not properly following procedures for verifying patient coverage, leading to corrective actions and reduced risk of claim rejections.

- Benefit: Properly managing financial risks and reducing the potential for legal actions or financial losses.

Limitations in the Healthcare Sector:

- Complex Billing and Reimbursement Structures:

- Application: Healthcare organizations often have complex billing systems with numerous payers, including private insurers, Medicare, and Medicaid. Auditing these systems can be challenging, particularly when reconciling payments and reimbursements from multiple sources.

- Example: An auditor may not be able to review every individual claim in detail, and errors or fraud in claims processing might go undetected if they are not part of the sample.

- Limitation: This may lead to undetected errors or fraud in billing practices, particularly in less scrutinized areas.

- Evolving Healthcare Standards:

- Application: Healthcare regulations are constantly evolving, and staying up-to-date with these changes can be challenging for auditors. New technologies and treatments can lead to complex billing scenarios that auditors may not fully understand.

- Example: Changes in the healthcare reimbursement policies for telemedicine services might not be fully accounted for in an audit, leading to potential non-compliance with new rules.

- Limitation: Auditors may struggle to keep up with evolving regulations, particularly in niche areas of healthcare or newer services like telemedicine.

Conclusion

Across various industries, the advantages of auditing—such as improved financial management, enhanced credibility, fraud prevention, and regulatory compliance—play a significant role in maintaining transparency and trust with stakeholders. However, industries must also recognize the limitations of auditing, such as sampling constraints, dependence on management information, and the complexity of specific industry-related transactions or systems.

To mitigate these limitations, industries need to complement auditing with robust internal controls, continuous monitoring systems, and employee training to ensure that they manage risks effectively and maintain financial accuracy.

Understanding how auditing’s advantages and limitations apply within specific industries is essential for businesses to leverage the full benefits of the audit process while addressing its potential shortcomings.

- Desk

- External

- Integrated

- Internal

- Party First-party

- Second-party

- Third-party

- Process

- Product

- Service

- System

- Academic

- Clinical

- Energy

- Financial

- Information

- Information technology Information security

- Quality

- Technical

- Aarhus Convention

- Climate justice

- Corporate accountability / behaviour / environmental responsibility / responsibility / social responsibility

- Dirty hands

- Environmental racism / in Russia / in the United States / in Western Europe / inequality in the UK / injustice in Europe

- Ethical banking

- Ethical code

- Extended producer responsibility

- Externality

- Harm

- Little Eichmanns

- Loss and damage

- Organizational ethics

- Organizational justice

- Pollution

- Principles for Responsible Investment

- Racism

- Social impact assessment

- Social justice

- Social responsibility

- Stakeholder theory

- Sullivan principles

- Transparency (behavioral

- social)

- UN Global Compact

- Corporate crime

- Double bottom line

- Ethical positioning index

- Higg Index

- Impact assessment (environmental

- equality

- social)

- ISO 26000

- ISO 45001

- Genuine progress indicator

- Performance indicator

- SA8000

- Social return on investment

- Whole-life cost

- Carbon accounting

- Eco-Management and Audit Scheme

- Emission inventory

- Environmental full-cost accounting / Environmental conflict / impact assessment / management system / profit-and-loss account

- ISO 14000

- ISO 14031

- Life-cycle assessment

- Pollutant release and transfer register

- Sustainability accounting / measurement / metrics and indices / standards and certification / supply chain

- Toxics Release Inventory

- Triple bottom line

- Global Reporting Initiative

- GxP guidelines

- Sustainability reporting

- Community-based monitoring

- Environmental (certification)

- Fair trade (certification)

- ISO 19011

- Bangladesh Accord

- Benefit corporation

- Child labour

- Community interest company

- Conflict of interest

- Disasters

- Disinvestment

- Eco-labeling

- Environmental degradation

- Environmental pricing reform

- Environmental, social, and corporate governance

- Ethical consumerism

- Euthenics

- Global justice movement

- Health impact assessment

- Market governance mechanism

- Product certification

- Public participation

- SDG Publishers Compact

- Social enterprise

- Socially responsible business

- Socially responsible investing

- Socially responsible marketing

- Stakeholder (engagement)

- Supply chain management

- Types of auditing

- Information science

References

- ^ Gupta, Kamal (November 2004). Contemporary Auditing. McGraw Hill. p. 1095. ISBN 0070585849.

- ^ “Audit assurance”.

- ^ PricewaterhouseCoopers. “What is an audit?”. PwC. Retrieved 2022-03-03.

- ^ Power, Michael (1999), The Audit Society: Rituals of Verification. Oxford: Oxford University Press.

- ^ Assurance, Auditing and. “Chapter 1”. ICAI – The Institute of Chartered Accountants of India. Vol. 1. Institute of Chartered Accountants of India. p. 1.

- ^ Loeb, Stephen E.; Shamoo, Adil E. (1989-09-01). “Data audit: Its place in auditing”. Accountability in Research. 1 (1): 23–32. doi:10.1080/08989628908573771. ISSN 0898-9621. PMID 26859053.

- ^ Derek Matthews, History of Auditing (2006-09-27). The changing audit process from the 19th century till date. Routledge-Taylor & Francis Group. p. 6. ISBN 9781134177912.

- ^ C. A., Moyer (January 1951). “Early Developments in American Auditing”. Accounting Review. 26 (1): 3–8. JSTOR 239850.

- ^ Johnson, H. Thomas (1975). “Reviewed work: A History of Accounting Thought, Michael Chatfield”. The Business History Review. 49 (2): 256–257. doi:10.2307/3113713. JSTOR 3113713. S2CID 154953655.

- ^ Mishra, Birendra K.; Paul Newman, D.; Stinson, Christopher H. (1997). “Environmental regulations and incentives for compliance audits”. Journal of Accounting and Public Policy. 16 (2): 187–214. doi:10.1016/S0278-4254(97)00003-3. Retrieved 1 April 2023.

- ^ Thottoli, Mohammed Muneerali (2021). “The relevance of compliance audit on companies’ compliance with disclosure guidelines of financial statements”. Journal of Investment Compliance. 22 (2). Emerald Insight: 137–150. doi:10.1108/JOIC-12-2020-0047. S2CID 236598426. Retrieved 1 April 2023.

- ^ McKenna, Francine. “Auditors and Audit Reports: Is The Firm’s “John Hancock” Enough?”. Forbes. Retrieved 22 July 2011.

- ^ “CONCEPT RELEASE ON POSSIBLE REVISIONS TO PCAOB STANDARDS RELATED TO REPORTS ON AUDITED FINANCIAL STATEMENTS” (PDF). Retrieved 22 July 2011.

- ^ “Auditing Standard No. 5”. pcaobus.org. Retrieved 2016-06-28.

- ^ Ladda, R.L. Basic Concepts Of Accounting. Solapur: Laxmi Book Publication. p. 58. ISBN 978-1-312-16130-6.

- ^ “Pages – Definition of Internal Auditing”. Na.theiia.org. 2000-01-01. Retrieved 2013-09-02.

- ^ “Pages – International Professional Practices Framework (IPPF)”. Na.theiia.org. 2000-01-01. Retrieved 2013-09-02.

- ^ “Professional internal auditors, in carrying out their responsibilities, apply COSO’s Integrated Framework-Internal Control”. Theiia.org.

- ^ Jump up to:a b Different Types of Audits (June 2013) Auditronix Guidance Note Archived July 18, 2013, at the Wayback Machine

- ^ Stanleigh, Micheal (2009). “UNDERTAKING A SUCCESSFUL PROJECT AUDIT” (PDF). PROJECT SMART. Retrieved 18 May 2016.

- ^ Clarke, Kevin; Walsh, Kathleen; Flanagan, Jack (21 December 2020). “How prevalent are post-completion audits in Australia”. Accounting, Accountability & Performance. 18 (2): 51–78.

- ^ Gilbert W. Joseph and Terry J. Engle (December 2005). “The Use of Control Self-Assessment by Independent Auditors”. The CPA Journal. Retrieved 10 March 2012.